Publication Date: May 2025 | Rwanda Tax & Advisory Series

Executive Summary

Rwanda just made one of its biggest changes to tax law in recent years. On 27 May 2025, the Government enacted Law No. 009/2025, which amends the existing VAT Law No. 049/2023. In simple terms: some goods and services that were previously tax-free are now subject to VAT (Value Added Tax), while certain strategic sectors still enjoy temporary tax relief.

What is VAT? VAT (Value Added Tax) is a consumption tax charged at 18% on most goods and services sold in Rwanda. It is collected by businesses on behalf of the government.

If you run a business in Rwanda — whether you are a truck driver, a phone retailer, a factory owner, a bank, or an electric vehicle company — this law affects you directly. This article breaks down exactly what has changed, what it means for your business in plain language, and the specific steps you need to take right now to stay legally compliant.

The Policy Rationale: Why Rwanda Reformed Its VAT Regime

Before diving into what changed, it helps to understand why the government made these changes. Rwanda's plan for managing government finances (called the Medium-Term Revenue Strategy, or MTRS) has always focused on collecting more tax money locally rather than relying too heavily on foreign aid or borrowing. VAT — charged at 18% on most goods and services — is one of the government's biggest sources of income. Zero-rated supplies (0% VAT) are special categories where no VAT is charged but businesses can still reclaim the VAT they paid on their own costs.

Several converging factors drove this reform:

Too many tax-free items ("Exemption creep"): Over the years, the government kept adding more and more goods and services to the tax-free list — often for good reasons at the time, but without reviewing whether those reasons still applied. For example, mobile phones were made VAT-free in 2010 to help more Rwandans afford them. But today, over 80% of Rwandans already have mobile phones. Keeping phones tax-free no longer serves the original purpose.

Hidden tax costs ("Revenue integrity"): When too many items are tax-free, it creates a problem called the "hidden VAT cost." Here is how it works: if your supplier pays VAT on materials but you are tax-exempt, you cannot reclaim that VAT — so it gets buried in your prices. By reducing the number of exemptions, the tax system becomes fairer and more transparent for everyone.

Smarter, time-limited incentives ("Sectoral targeting"): Instead of broad, permanent tax-free lists, the government now wants targeted tax breaks with clear deadlines and clear goals. For example, electric vehicles get a VAT exemption until 2028 to encourage green transport — but the exemption will be reviewed and may not continue after that date.

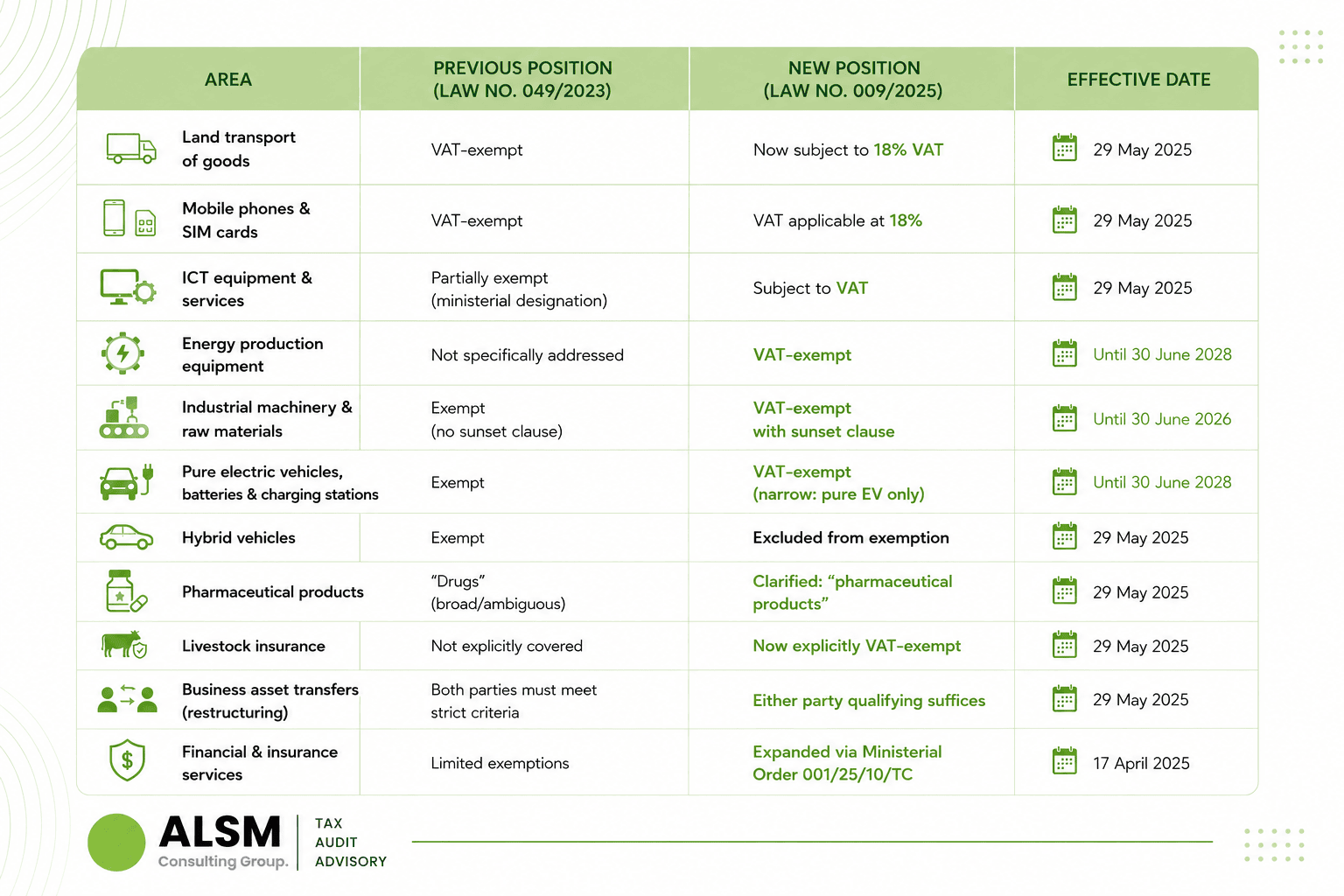

Key Amendments at a Glance

The table below summarises the principal changes introduced by Law No. 009/2025 compared to the preceding Law No. 049/2023:

Sectoral Deep-Dive: Who Is Most Affected?

Logistics and Distribution Sector

In plain terms: if your business moves goods by road — as a truck driver, a delivery company, or a distribution firm — you must now add 18% VAT to what you charge your customers. This is new. Previously, transporting goods by road was tax-free. That exemption has now been removed.

What this means in practice:

Check your existing contracts: If you signed a transport agreement before 29 May 2025 that did not include VAT, you will need to talk to your client about who pays the new 18% VAT — you or them. This should be agreed in writing.

There is a silver lining: Previously, transport companies could not reclaim the VAT they paid on fuel, tyres, or vehicle repairs. Now that you charge VAT, you can also reclaim ("recover") the VAT you paid on your own business costs — which can meaningfully reduce your overall expenses.

What is Input VAT? Input VAT is the VAT your business pays when buying goods or services for its operations. If you charge VAT to your customers (Output VAT), you can subtract what you already paid (Input VAT) and only hand the difference to RRA.

Do you need to register for VAT? You must register if your annual sales exceed RWF 20,000,000 (about RWF 1.67M per month). Once registered:

• If your annual turnover is below RWF 200,000,000 — file VAT returns every 3 months (quarterly).

• If your annual turnover is above RWF 200,000,000 — file every month.

Immediate action: Logistics firms must update EBM (Electronic Billing Machine) configurations, revise customer invoicing templates, and engage finance teams on price adjustments or contractual renegotiation.

ICT and Telecommunications Sector

If you sell, import, or distribute mobile phones, SIM cards, computers, or other tech equipment in Rwanda, these items are no longer VAT-free. You must now charge 18% VAT on these products.

The government's reasoning: mobile phone ownership in Rwanda has grown strongly over the past 15 years. The original goal of the tax exemption — to make phones more affordable and accessible — has largely been achieved. International bodies like the IMF and World Bank also advised Rwanda to reduce the number of tax-exempt items, as too many exemptions can weaken the tax system.

Businesses in this sector should consider:

Decide how to handle the new VAT on prices: Will you absorb the 18% VAT yourself (reducing your profit margin) or add it to customer prices? Either way, update your supplier agreements and customer price lists accordingly.

VAT registration reviews: distributors, retailers, and importers who previously fell below registration thresholds due to exempt turnover may now cross the RWF 20,000,000 mandatory registration threshold.

Input VAT recovery planning: Historically exempt ICT operators may now be eligible to deduct input VAT on their purchases — a cost optimisation opportunity that should be modelled immediately.

Manufacturing and Industrial Sector

Good news for factory owners and manufacturers: machinery and raw materials you import for industrial use are still VAT-free — but only until 30 June 2026. After that date, unless the government extends the exemption, you will need to pay 18% VAT on those imports.

What is a "sunset clause"? A sunset clause means a tax benefit has an expiry date. After that date, the benefit automatically ends unless the government renews it. This gives businesses time to plan but also means you must act before the deadline.

Buy your equipment now, not later: If you are planning to purchase new factory machinery or industrial equipment, try to complete those purchases before 30 June 2026 to take advantage of the VAT-free status. Waiting until after that date could cost you an extra 18% on every purchase.

Make sure your imports are correctly labelled: When importing equipment, the customs code (called a tariff classification) assigned to your goods must correctly identify them as industrial equipment — otherwise Rwanda Customs may refuse the VAT exemption. Incorrect labeling is one of the most common reasons businesses lose their exemption at the border. Work with a licensed clearing agent or tax advisor to get this right.

Sunset contingency planning: Finance teams should model the VAT cost impact post-June 2026 and incorporate this into multi-year business cases and investment analyses.

Energy Sector

If your business is involved in producing or supplying electricity — for example, as a solar panel importer, grid developer, or power producer — your equipment is VAT-free until 30 June 2028. This exemption supports Rwanda's national goal of bringing electricity to every home and business in the country.

The practical impact:

Solar equipment importers, grid infrastructure developers, and independent power producers (IPPs) operating in Rwanda can all leverage this exemption.

If you have a project budget or investment plan in the energy sector that assumed VAT costs on equipment, update those numbers — you may have been over-estimating costs. This is particularly relevant for public-private partnership (PPP) projects where every cost line matters.

E-Mobility Sector

Important change for vehicle buyers and fleet managers: the VAT exemption now applies only to fully electric vehicles (cars, motorbikes, or buses powered entirely by a battery). Hybrid vehicles — those that run on both electricity and petrol — no longer qualify for the exemption and are now subject to 18% VAT.[cite:page:1][cite:7]

Why? The government wants to push Rwanda towards fully electric transport rather than partly electric (hybrid) options. The VAT exemption for pure EVs runs until 30 June 2028 — giving individuals, businesses, and transport companies a clear window to make the switch to electric at a lower cost.

⚠️ Special case — locally assembled vehicles: Electric and hybrid vehicles that are assembled inside Rwanda (not imported fully built) are treated differently — they are "zero-rated" (0% VAT, but the manufacturer can still reclaim their input VAT costs). This makes locally assembled EVs more financially attractive than imported ones, even hybrids.

Financial and Insurance Services

Banks, insurance companies, and microfinance institutions (MFIs) get expanded VAT exemptions under a new Ministerial Order (No. 001/25/10/TC, dated 16 April 2025). In simple terms, more of what these businesses do is now clearly tax-free — reducing the confusion that previously existed about what should and should not attract VAT in the financial sector.

Key exempt financial services under the Order include:

Core banking services (deposit-taking, lending, payment processing)

Insurance products and risk management services

Microfinance services

Livestock and agricultural insurance — now explicitly exempt under the amended law.

However, financial institutions often do both taxable and tax-free services. In those cases, you must split ("apportion") your input VAT costs between the two types of activities. Only the portion linked to taxable services can be reclaimed from RRA. Your tax advisor or RRA can help you calculate the correct split.

Business Restructuring: A Welcome Simplification

If you are buying or selling a business in Rwanda, the new law makes this easier from a VAT perspective.

Previously, to avoid paying VAT on a business sale, both the seller AND the buyer had to meet a strict set of conditions. The new rule is more flexible: the VAT exemption now applies as long as either the buyer has been in business for at least 3 years, OR the seller mainly deals in VAT-exempt goods. You no longer need both parties to qualify.

This is helpful if you are:

Buying or merging with another Rwandan company

Reorganising your group of companies internally (e.g. moving assets between subsidiaries)

Buying a business from the government (privatisation)

In all these cases, the VAT paperwork has been simplified.

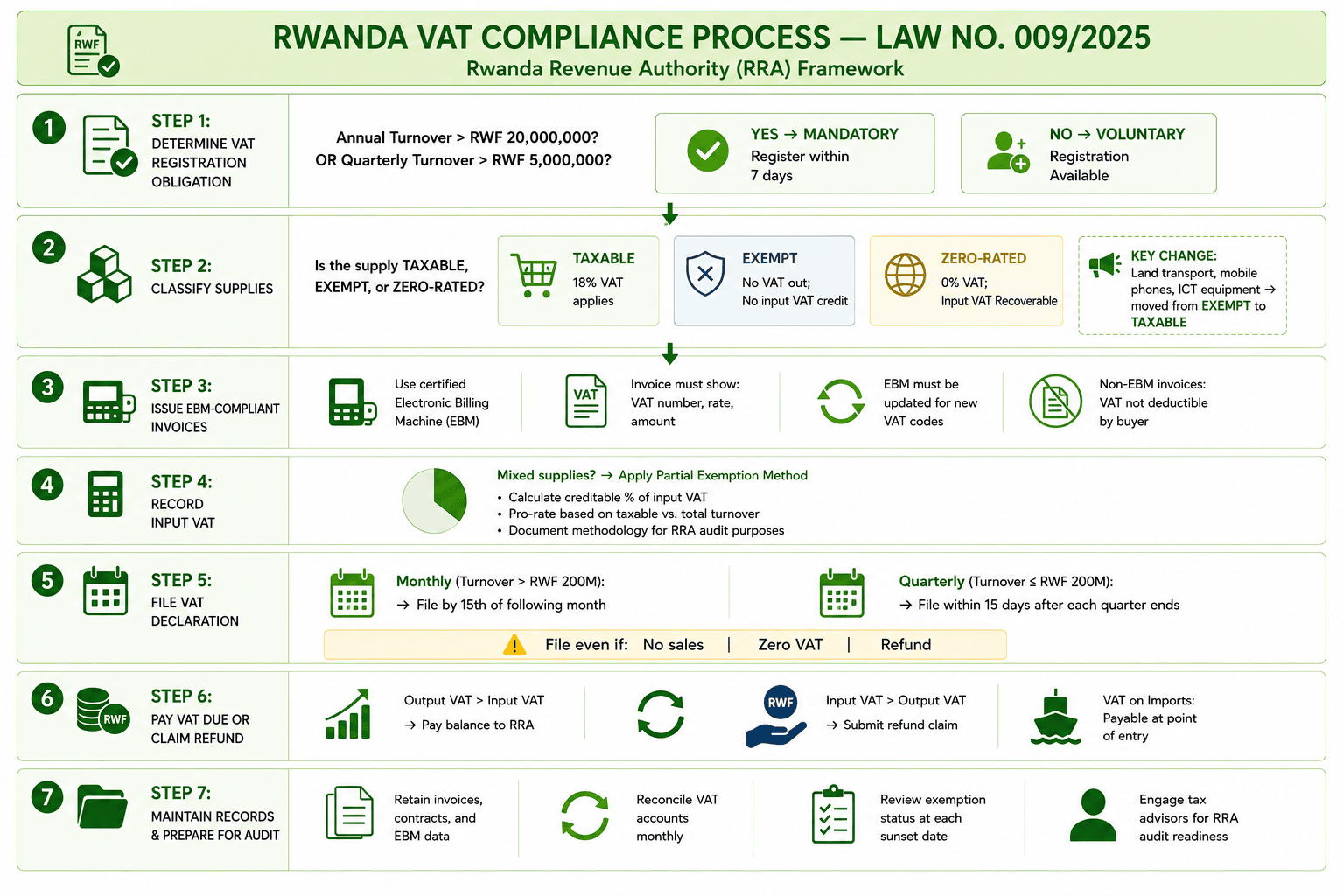

VAT Compliance Process: Step-by-Step Framework

The flowchart below illustrates the end-to-end VAT compliance process for businesses operating in Rwanda under the reformed framework.

Source: Rwanda Revenue Authority (RRA) | Law No. 009/2025 | Law No. 049/2023

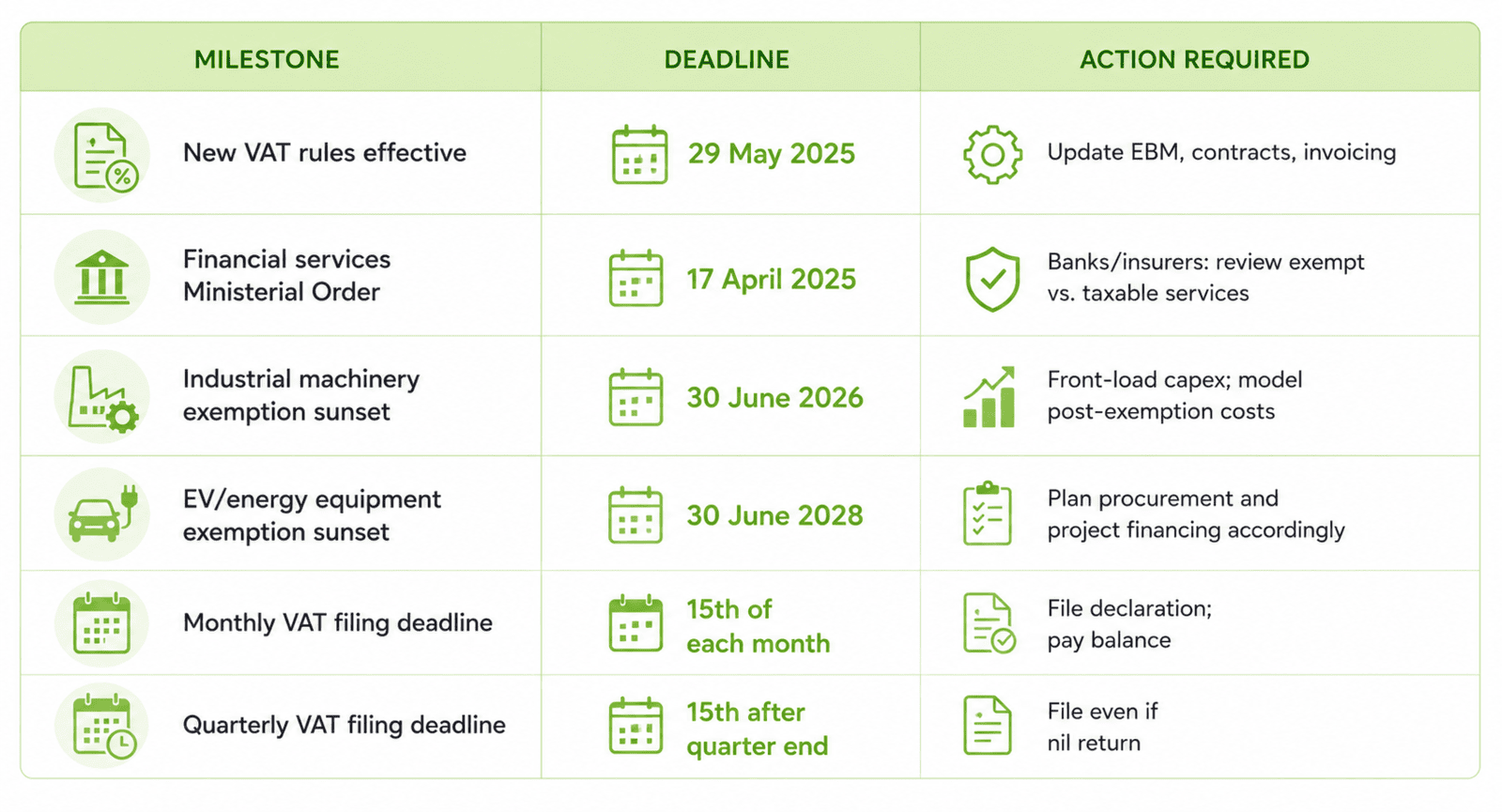

Critical Compliance Dates: Your Action Calendar

VAT Reward Scheme: An Often-Overlooked Incentive

Did you know RRA pays customers cash back for asking for receipts? The VAT Reward Scheme is a government initiative that gives a portion of the VAT paid back to consumers who request an official EBM (Electronic Billing Machine) receipt. In other words: your customers are financially rewarded for asking you for a proper receipt — which means they will.

The practical implications for businesses are significant:

What this means for your business: When customers expect and ask for EBM receipts, it becomes much harder to operate informally or skip proper invoicing. This protects you from penalties — and builds trust with your customers.

RRA can see everything: Every EBM receipt issued creates a transaction record at RRA. This means RRA knows how much you should be collecting in VAT. Businesses that do not issue proper EBM receipts are more likely to be flagged for a tax audit.

Consumers can register via or through the Myrra system to participate.

Implications for Financial Reporting under IFRS

If your company follows international accounting rules (IFRS — International Financial Reporting Standards, the standard used by listed companies and large businesses in Rwanda), the new VAT law also affects how you record numbers in your accounts. Here is what your finance team or accountant needs to know:

Stock and goods on your shelves (IAS 2 — Inventories): If your business can no longer reclaim some or all VAT on items you buy to sell, that unrecoverable VAT becomes part of your cost price. This will reduce your profit margin on those goods.

Equipment and machinery (IAS 16 — Fixed Assets): If you cannot reclaim VAT on a machine or piece of equipment you buy, that VAT cost must be included in the purchase price of the asset in your books. Because you depreciate (write off) the asset over time, this will increase your annual depreciation charge and reduce your reported profit.

Past tax risks (IAS 37 — Provisions): If your business previously treated certain sales as VAT-exempt but they are now taxable, RRA could assess you for unpaid VAT going back in time. Your accountant needs to review whether this is a risk and, if so, set aside a provision (a reserve) in your accounts to cover a possible payment.

Revenue contracts (IFRS 15 — Revenue Recognition): If the new VAT rules force you to change a contract with a customer — for example, by adding VAT to a previously VAT-free service — this may count as a formal contract modification under accounting rules. Your accountant will need to review whether this affects how and when you recognize revenue in your financial statements.

Action point: Talk to your external auditor (the firm that signs off your accounts) as soon as possible about how these VAT changes will be reflected in your June 2025 financial statements.

Ten Actionable Recommendations for Businesses

Here is a practical checklist of the 10 most important actions every business in Rwanda should take following this new law:

Conduct an immediate VAT supply classification review: Map all goods and services supplied or procured against the revised exemption schedule in Law No. 009/2025. Identify supplies that have moved from exempt to taxable.

Update EBM configurations without delay: Ensure your Electronic Billing Machine reflects new VAT codes for previously exempt supplies now subject to 18% VAT — particularly land transport, mobile phones, and ICT equipment.

Renegotiate affected contracts: Transport, ICT service, and distribution contracts signed under the previous regime may not account for VAT. Engage counterparties promptly on price adjustment mechanisms or VAT absorption clauses.

Optimise input VAT recovery: Where your business moves from exempt to taxable status, you gain the right to recover input VAT on related costs. Quantify this benefit and factor it into pricing strategies.

Handle mixed VAT correctly: If your business sells both taxable and VAT-exempt goods or services, you cannot reclaim all of your input VAT — only the portion that relates to your taxable sales. Calculate this split accurately and keep all supporting records in case RRA audits you.

Front-load capital expenditure in manufacturing: If industrial machinery procurement is planned, accelerate it before the 30 June 2026 sunset on industrial machinery exemptions.

Plan your electric vehicle purchases by 2028: If you manage a vehicle fleet or run an e-mobility business, plan to buy pure electric vehicles before the VAT exemption expires on 30 June 2028. After that date, those vehicles will likely cost 18% more.

Assess accounting impacts: Ask your finance team or accountant to review how the new VAT rules affect your financial statements — particularly your cost of goods, asset values, and any past-year tax risks. This should be done before preparing your June 2025 accounts.

Leverage the VAT Reward Scheme: Ensure all customer-facing staff understand the EBM invoicing obligation and educate customers on their right to demand EBM receipts — reducing your exposure to compliance penalties.

Engage specialist tax advisors for an impact assessment: The breadth of this reform warrants a formal, sector-specific tax impact assessment. An experienced tax advisory firm can identify both risks and opportunities that a self-assessment may miss.

Conclusion:

Rwanda's new VAT law is not just a technical tweak — it is a signal of where the government is heading. The days of broad, permanent tax exemptions are over. Going forward, tax breaks will be targeted, time-limited, and tied to clear national goals. The message from the Ministry of Finance (MINECOFIN) and Rwanda Revenue Authority (RRA) is straightforward: if a tax exemption no longer serves a purpose, it will be removed.

For business owners and managers, the message is equally direct: doing the bare minimum is no longer enough. The businesses that will thrive are those that understand their new VAT obligations, claim back every franc of input VAT they are entitled to, and update their contracts and pricing strategies to reflect the new rules.

Rwanda's tax rules will keep changing. Businesses that stay informed, work with qualified tax advisors, and keep their compliance systems up to date will avoid costly penalties — and will be better positioned than competitors who react too late. Start today.

This article has been prepared for informational purposes and reflects the law as at May 2025. It does not constitute legal or tax advice. For advisory support, contact us at : info@alsm.ltd or WhatsApp +250 784 441 144

Sunny MATETI

Managing Partner

Chartered Accountant and Certified Public Accountant, I excel in managing intricate tasks, adhering to strict deadlines, and providing outstanding results. My expertise is grounded in a solid 17+ years of experience in auditing, accounting, tax, and advisory services.

Need help adapting to the new VAT law?

Let ALSM Ltd’s experts guide your compliance and tax planning strategy.